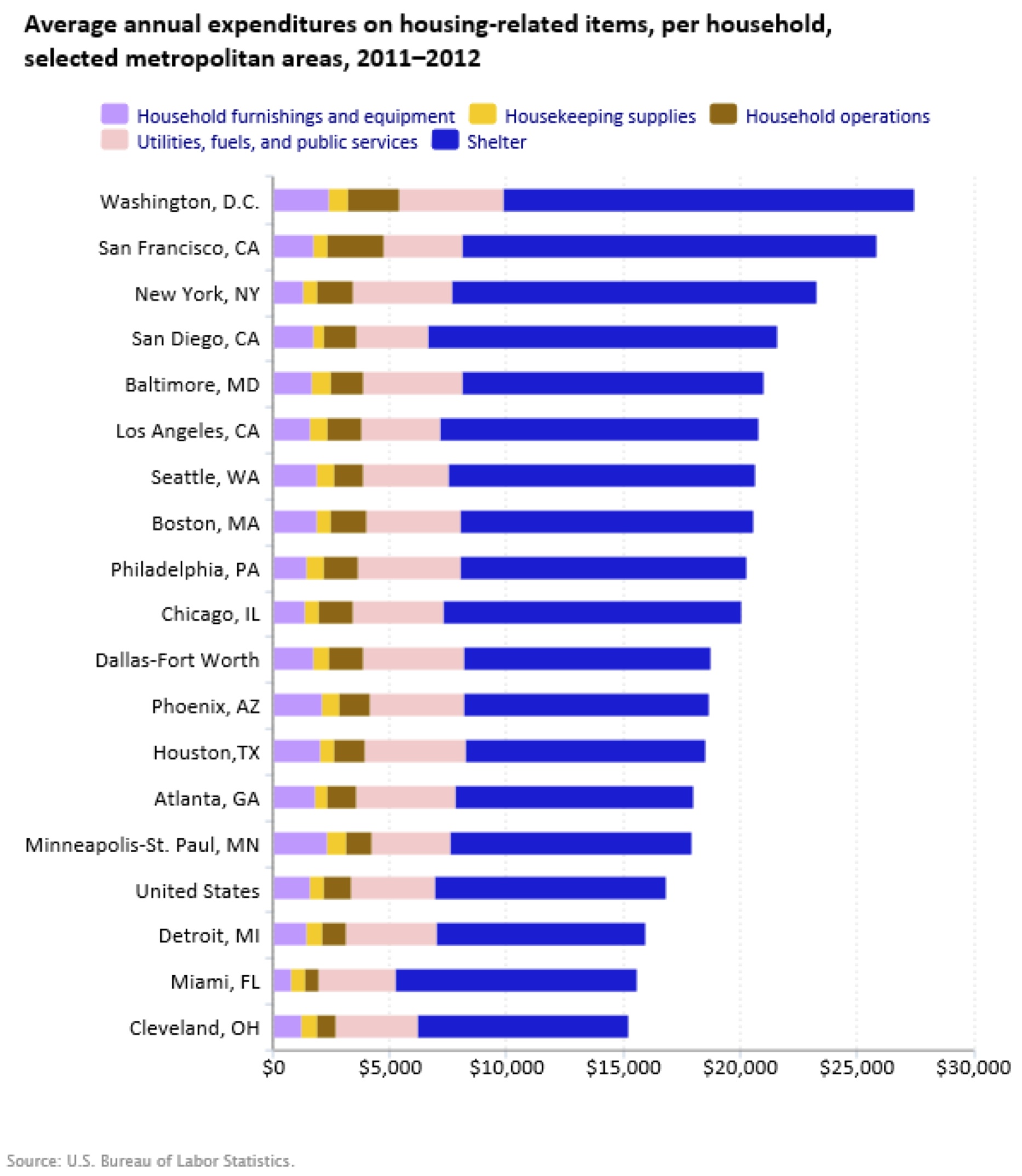

The Washington region is now the most expensive place to live in the country, ahead of New York and San Francisco, according to a recent study by the Bureau of Labor Statistics. We spend more on housing and related expenses. – The Washington Post.

The Washington region is now the most expensive place to live in the country, ahead of New York and San Francisco, according to a recent study by the Bureau of Labor Statistics. We spend more on housing and related expenses. – The Washington Post.

The median price if a single family home sold in DC last month was $620,000 up 3.3% from a year ago. The median condo price was $410,000 up just 1% since last September – according to GCAAR, the Greater Capital Area Assoc. of Realtors. More homes are on the market, so there is more to choose from. To read more click here.

From low down payment options to jumbo loan options for move-up buyers, here’s what a few lenders are offering buyers.

Chase’s DreaMaker loan is geared for low to moderate income borrowers and first time buyers. Funds are available for up to 95% of the home’s value and there is no upfront PMI (Private Mortgage Insurance). In some cases this might be cheaper than an FHA loan.

Chase just introduced jumbo loans with a maximum 85% LTV. With a 740 FICO score, the maximum loan amount is $1.5 million.

Guaranteed Rate is offering 80-10-10 jumbo loans of up to $1 million. You’d put down 10% of the home’s value, with a mortgage for 80% and a second mortgage for the remaining 10%. This would require about 1/8 % more in your interest rate.

HomeTrust Mortgage Corp is offering a Launch Loan. The loan requires only 5% down (which can be a gift), and the PMI will be waived for a nominally higher interest rate os 1/8 to 1/4 %. This can considerably lower monthly payments.

You can read more about this by clicking here.

A higher credit score means better loan options with better rates, that lower your payments and save you money. Your credit score is determined by: payment history, amounts owed, length of credit history, new credit, and types of credit used.

FIVE WAYS TO IMPROVE YOUR CREDIT SCORE